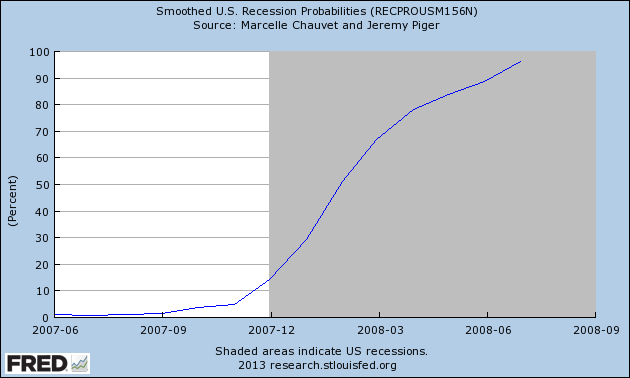

Probability of another recession: 1.34% according to the Federal Reserve Bank of St. Louis

Economists at the St. Louis Fed periodically estimate the probability of a U.S. recession. The econometric model that they use incorporates monthly data on non-farm payroll employment, industrial production, personal income, manufacturing sales, and trade sales. The model was fairly successful at predicting the most recent recession in 2008. See graph below.

U.S. Recession Probabilities

http://research.stlouisfed.org/fred2/series/RECPROUSM156N?cid=33120

2013-07: 1.34 Percent

| 2013-06: | 0.66 | |

| 2013-05: | 0.36 | |

| 2013-04: | 0.58 | |

| 2013-03: | 0.44 |

Monthly, Not Seasonally Adjusted, Updated: 2013-10-01 8:11 AM CDT

Details:

Smoothed recession probabilities for the United States are obtained from a dynamic-factor markov-switching model applied to four monthly coincident variables: non-farm payroll employment, the index of industrial production, real personal income excluding transfer payments, and real manufacturing and trade sales. This model was originally developed in Chauvet, M., “An Economic Characterization of Business Cycle Dynamics with Factor Structure and Regime Switching,” International Economic Review, 1998, 39, 969-996. (http://faculty.ucr.edu/~chauvet/ier.pdf)

For additional details, including an analysis of the performance of this model for dating business cycles in real time, see:

Chauvet, M. and J. Piger, “A Comparison of the Real-Time Performance of Business Cycle Dating Methods,” Journal of Business and Economic Statistics, 2008, 26, 42-49.

(http://pages.uoregon.edu/jpiger/cp_realtime_2_020907.pdf)

For additional details as to why this data revises, see FAQ 3 athttp://pages.uoregon.edu/jpiger/us_recession_probs.htm.

Related Posts

Posted by Matt Rigling | U.S. Economy

STATA statistical code for estimation of Millimet et al. (2002) econometric worklife model

The STATA code for estimating the Millimet et a;. (2002) econometric worklife model can be found below. The code will need to be adjusted to fit your purposes. However, the […]

Posted by Matt Rigling | U.S. Economy

A narrative description of the Millimet et. al (2002) econometric worklife model

The following describes the approach used by Millimet et al (2002) to estimate U.S. worker worklife expectancy. The pdf version can be found here: Millimet (2002) Methodology Description Methodology First, transition […]

Posted by Matt Rigling | U.S. Economy

Big BLS employment data, disability, and worklife expectancy

Big Data. Bureau of Labor Statistics. Survey data. Employment Big Data. Those are all things that calculating worklife expectancy for U.S. workers requires. Worklife expectancy is similar to life expectancy and […]

Posted by Matt Rigling | BLS Data | Earnings | Industry | U.S. Economy | Wage and hour cases

FLSA OT report for individuals working in Derrick, rotary drill, and services unit operators, oil, gas, and mining occupations

In this post, we look at the weekly overtime (OT) hours typically worked by those who work in Derrick, rotary drill, and services unit operators, oil, gas, and mining occupations. Many […]

Posted by Matt Rigling | U.S. Economy

Younger workers today have slightly less attachment to the workforce than younger workers in the past

Big Data. Bureau of Labor Statistics. Survey data. Employment Big Data. Those are all things that calculating worklife expectancy for U.S. workers requires. Worklife expectancy is similar to life expectancy and […]

Posted by Matt Rigling | BLS Data | Job openings | U.S. Economy

Elementary and Middle School Teachers experienced the largest increase of job openings nationwide for Dec

Elementary and Middle School teachers experienced the largest increase of new openings of all occupations in the US for the month of December with 4,017 new job openings. Month Occupation […]

Posted by Matt Rigling | U.S. Economy

Replication of the Millimet et al. (2002) work was sufficient and yielded similar results

Big Data. Bureau of Labor Statistics. Survey data. Employment Big Data. Those are all things that calculating worklife expectancy for U.S. workers requires. Worklife expectancy is similar to life expectancy and […]

Posted by Matt Rigling | BLS Data | Job openings | U.S. Economy

Tallahassee, FL experienced largest increase in job openings of all US MSAs for Dec

The Tallahassee, FL MSA (metropolitan statistical area) experienced the largest increase of job openings of all MSAs in the United States for the month of December with 155 new openings. Month MSA Total […]

Posted by Matt Rigling | BLS Data | Earnings | Industry | U.S. Economy | Wage and hour cases

FLSA OT report for individuals working in roofing occupations

In this post, we look at the weekly overtime (OT) hours typically worked by those who work in roofing occupations. Many of the employees that work in these jobs are not exempt […]

Posted by Matt Rigling | U.S. Economy

Steward and Gaylor (2015) Matched CPS Sample Sizes for 1993-2013 time period

Big Data. Bureau of Labor Statistics. Survey data. Employment Big Data. Those are all things that calculating worklife expectancy for U.S. workers requires. Worklife expectancy is similar to life expectancy and […]